Series – II – What are the next steps for entrepreneurs?

May 2020 • Subrina Shrestha, MSME and Agri Finance Consultant (BFC, Nepal)

This article is the second part of the article published in April 2020 which was accompanied by a short survey. A total of 35 respondents were interviewed to obtain a general overview of the entrepreneurs’ perception and actions expected to be taken due to the COVID-19 crisis.

In Nepal, the elongated lockdown measure has resulted in a general environment of increased discomfort among businesses, and a restlessness among citizens evident by increased cases of people being held for defying the lockdown orders. The gradual (phased) lifting of the lockdown is bound to happen sooner than later. And when that happens, it won’t be back to business as usual. Revenue rebound for most businesses is expected to be slow, while cost continues to pile up and venturing into the unknown post COVID economy will compel businesses to take harsh steps.

Insights from the Survey

Recovery Mode On

The principal action for businesses will be to change gears from panic mode to recovery mode. It will be important to understand the damage done in terms of key numbers – cash flow, cost of cancelled contracts, etc. without being swayed by the negative bias around survival of businesses in a post Covid economy. The level of impact on businesses will be different depending on the sector and also on how the business model was or will be pivoted to adjust to the challenges of Covid. Stories of how perishable agri-goods are rotting in the fields are abundant amidst this crisis while on the other hand a few organized agri-based companies such as Mato, AgriMove, and Kheti are advertising their ability to supply fresh fruits and vegetables in Kathmandu. Flexibility and innovation in the way of doing business will allow smart entrepreneurs to prevail.

Staff Management and Pay Revisions

During the time of crisis, the decisions taken by businesses are bound to be scrutinized by the public. But the harsh reality is that businesses, in order to remain afloat, have to take strategic decisions that may result in layoffs and pay cuts. Adopting a lean management structure would be key to remaining effective during this time, and also providing an opportunity to consider innovative ways to manage staff would be beneficial.

Nossa pesquisa mostrou que as três principais ações que foram forçadas a serem tomadas devido à restrição de quarentena, estavam 1) reduzindo o salário/salário dos funcionários, 2) diminuindo a escala dos negócios e 3) reduzindo o número de funcionários. É imperativo que, se as empresas decidirem diminuir, uma série de posições atuais será desnecessária ou inacessível, resultando em mais cortes da equipe. A opção atual amplamente adotada de reduzir os salários também deve ser estratégica, pois um corte de salário percentual plano pode ser uma proposta arriscada quando comparada a um corte percentual de salto em suporte de ganho (abordagem de baixo para cima), que garante uma receita básica de sobrevivência para os membros da equipe de ganhos mais baixos. Embora os cortes salariais possam ser inevitáveis, as empresas também precisam criar estratégias sobre como reter e motivar a equipe. Opções como licença sabática de curto prazo e pagamentos diferidos (horários acumulados a serem reivindicados durante os dias úteis regulares) também podem ser explorados. A revisão de salário descendente também precisa ser revisada para cima como e quando a situação melhorar, a falha em fazê -lo pode resultar na perda de recursos humanos importantes.

lidando com a queda da demanda

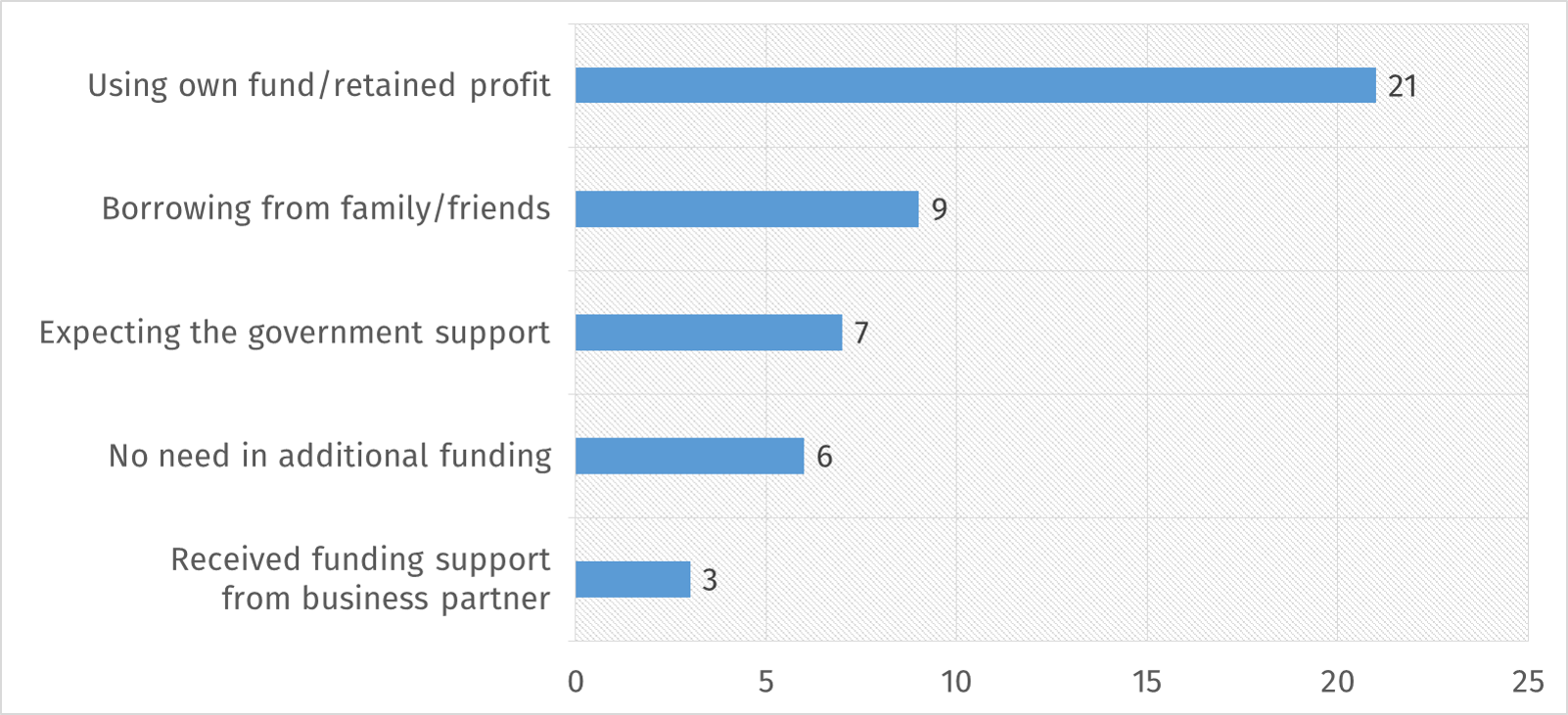

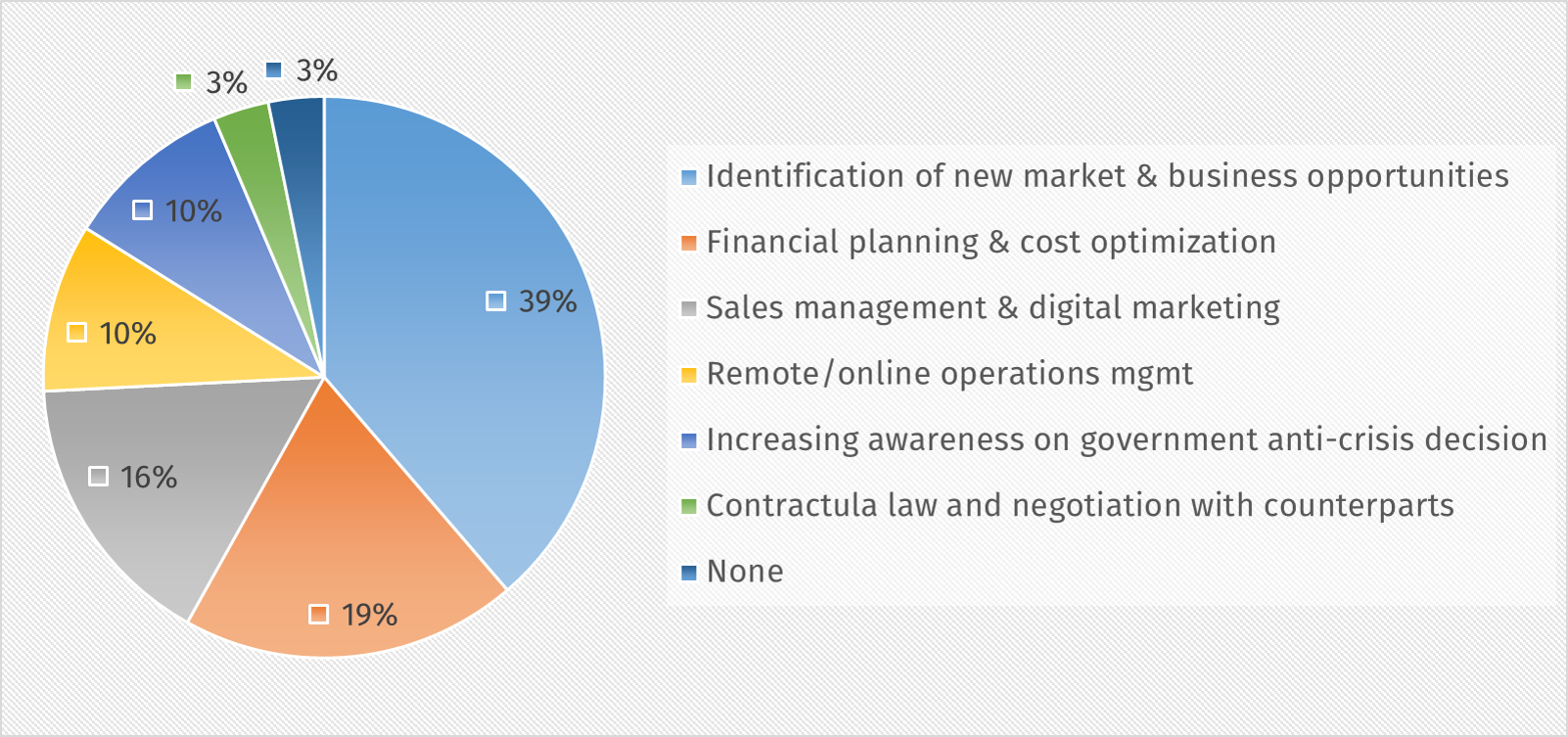

Houve um acordo geral entre os entrevistados de que a demanda doméstica e estrangeira cairá, com a expectativa de atraso na entrega de produtos/serviços para continuar. A recuperação, pós-Covid, deve ser lenta (recuperação em forma de U), em comparação com a recuperação testemunhada após o aquecimento de 2015. Uma queda prolongada na demanda impulsionará a sobrevivência dos negócios, e mais ainda para aqueles com baixas reservas de caixa. Embora girar o modelo de negócios deva ser uma ênfase importante para as empresas, algumas tendências podem ser temporárias e as empresas não devem ser influenciadas pelas tendências de curto prazo alimentadas pela crise. É essencial analisar qual comportamento provavelmente será uma mudança comportamental sustentada entre clientes e funcionários. descontos de taxa de juros e adiamento da data de pagamento de impostos. Nossa pesquisa mostrou que, mesmo no tempo da crise, a maioria dos entrevistados (60%) preferia usar seu próprio fundo/lucro retido para manter seus negócios, essa preferência foi relatada em combinação com empréstimos de familiares, amigos e parentes (25,7%) e financiamento de apoio de parceiros de negócios (8,6%). A hesitação em fazer financiamento bancário parece ser persistente em situações de crise. Isso, no entanto, não deve ser uma surpresa, pois a pesquisa do NRB nas PMEs mostrou que apenas 16% das PME financiam seu capital inicial por meio de empréstimos bancários. É essencial observar que 20% dos entrevistados esperam apoio do governo para resistir a essa crise. exposição. Olhando para os programas introduzidos por outros governos, como o empréstimo de emergência Covid-19 de pequenas empresas dos EUA, o esquema de incentivos fiscais do governo indiano para pequenas empresas e incentivos para a manufatura doméstica etc. pode ser uma boa fonte de informação sobre o que o governo pode fazer e as lições sobre quais são as questões, assim como os desafios da implementação. Assim, o governo poderia aproveitar uma vantagem de segundo lugar sobre isso. Não há dúvida de que a economia do Nepal precisará de seu próprio pacote de alívio personalizado para abordar as preocupações da economia, sem esquecer as pequenas empresas que variam da agricultura à fabricação. Crise e garantir a sobrevivência dos negócios, os empreendedores também buscam intervenção não financeira na forma de atividades de capacitação. Nossa pesquisa mostrou que os empreendedores também estão procurando intervenções de capacitação, com as três principais áreas identificadas - identificação de novas oportunidades de mercado e negócios, planejamento financeiro e otimização de custos e gerenciamento de vendas e marketing digital. Projetos financiados por doadores podem aproveitar esta oportunidade para criar treinamento e atividades em torno da capacitação para melhorar a capacidade dos empreendedores de enfrentar a crise. foto. Não é hora de tomar decisões de pânico, mas se concentrar na inovação e na sobrevivência. Não há especialistas nessa incerteza e empreendedores por todo o lado estão rapidamente girando e inovando para sustentar negócios. Os empreendedores também precisam defender ativamente o apoio necessário e expressar sua opinião, pois o governo também está sobrecarregado gerenciando a crise. Cobrindo áreas como alfabetização financeira e gestão de negócios, a Sedra superou a equipe de sua empresa parceira Shreenagar Agro Farm e forneceu o kit de ferramentas de treinamento necessário, permitindo que eles continuem com atividades de treinamento mesmo após o final do projeto. Da mesma forma, com a identificação da falta de informações como uma questão -chave, a Sedra também apoiou seus bancos parceiros (Global IME Bank e NMB Bank) no Nepal para desenvolver boas práticas agrícolas e folhetos de capacitação e kits de ferramentas para agricultores comerciais. No cenário atual, a BFC iniciou um pacote de resposta CoVID-19, no qual a equipe de especialistas bancários da BFC fornece webinars gratuitos sobre resposta de crises e consultas de resposta de praticar banqueiros em seu

“Since we are in the travel industry, the entire year of 2020 doesn’t look good for us. People may not be willing to travel immediately even if the COVID situation improves”

Stimulus package/relief programs

The government so far has only introduced relief packages for businesses in the form of interest rate discounts and tax payment date deferral. Our survey showed that, even in the time of crisis, the majority of the respondents (60%) preferred to use their own fund/retained profit to maintain their business, this preference was reported in combination with borrowing from family, friends and relatives (25.7%) and funding support from business partners (8.6%). Hesitation to take bank financing appears to be persistent in crisis situations. This, however, should not come as a surprise as the NRB survey on SMEs had shown that only 16% of SMEs finance their initial capital through bank loans. It is key to note that 20% of respondents are expecting support from the government to weather this crisis.

Top 5 funding conditions preferred by businesses during COVID crisis (multiple choice)

It is clear that the current support, in terms of interest rate, is likely to cover only a fraction of businesses and in some cases could be more of a missed chance for businesses with prudent financial management, high cash reserve cushion and low bank loan exposure. Looking at the programs introduced by other governments such as the US’s Small Business COVID-19 Emergency Loan, the Indian government’s scheme of tax breaks for small businesses and incentives for domestic manufacturing, etc. could be a good source of information on what the government can do and lessons on what the issues are, as well as, challenges in implementation. So the government could leverage on some second-mover advantage on this. There is no doubt that Nepal’s economy will need its own tailored relief package to address the concerns of the economy while not forgetting about the small enterprises ranging from agriculture to manufacturing.

“Our goods are stranded at the custom points since the last three months, leading to diminishing value of inventory and increased costs”

Capacity Building Support

In order to sustain the crisis and ensure survival of the business, entrepreneurs also seek non-financial intervention in the form of capacity building activities. Our survey has shown that entrepreneurs are also looking for capacity building interventions with the top three identified areas being – Identification of new market & business opportunity, Financial Planning & Cost Optimization, and Sales Management & Digital Marketing. Donor funded projects could take this opportunity to devise training and activities around capacity building to enhance the capacity of entrepreneurs to weather the crisis.

Capacity building intervention sought by entrepreneurs

“Every industry still seems to be unknown about the daily consumption of their respective produce”

In a time of crisis it is easy to fail to see any positivity and lose sight of the bigger picture. It is not the time to make panic decisions but to concentrate on innovation and survival. There are no experts on this uncertainty and entrepreneurs all over are rapidly pivoting and innovating to sustain business. Entrepreneurs have to also actively advocate on the support that they require and voice their opinion as the government is also overwhelmed managing the crisis.

BFC in the implementation of KfW funded Sustainable Economic Development in Rural Areas in Nepal (SEDRA) has been providing capacity building trainings to MSMEs and agri-entrepreneurs. Covering areas such as Financial Literacy and Business Management, SEDRA upskilled the staff of its partner company Shreenagar Agro Farm and provided the required training toolkit, enabling them to continue with training activities even after the end of the project. Similarly, with the identification of lack of information as a key issue, SEDRA also supported its partner banks (Global IME Bank and NMB Bank) in Nepal to develop Good Agriculture Practices leaflets and capacity building toolkits for commercial farmers. In the current scenario, BFC has started a COVID-19 response package within which BFC’s team of banking experts provide free webinars on Crisis Response and answer queries from practicing bankers in its Ask BFC q & A Series.